By Phil Slinger – CAB CEO

The UK’s Construction Industry is subject to turbulent times at the moment, along with the state of the economy. With a forecasted drop in construction output for 2023, it is expected that growth will return in 2024. So currently, as economic inflation seems to be easing, have we seen the worst of the dip in our Construction Industry, or is there worst to come in 2023?

Reviewing CAB’s State of Trade Survey produced alongside other construction products output by the CPA (Construction Products Association) there may be a glimmer of light ahead.

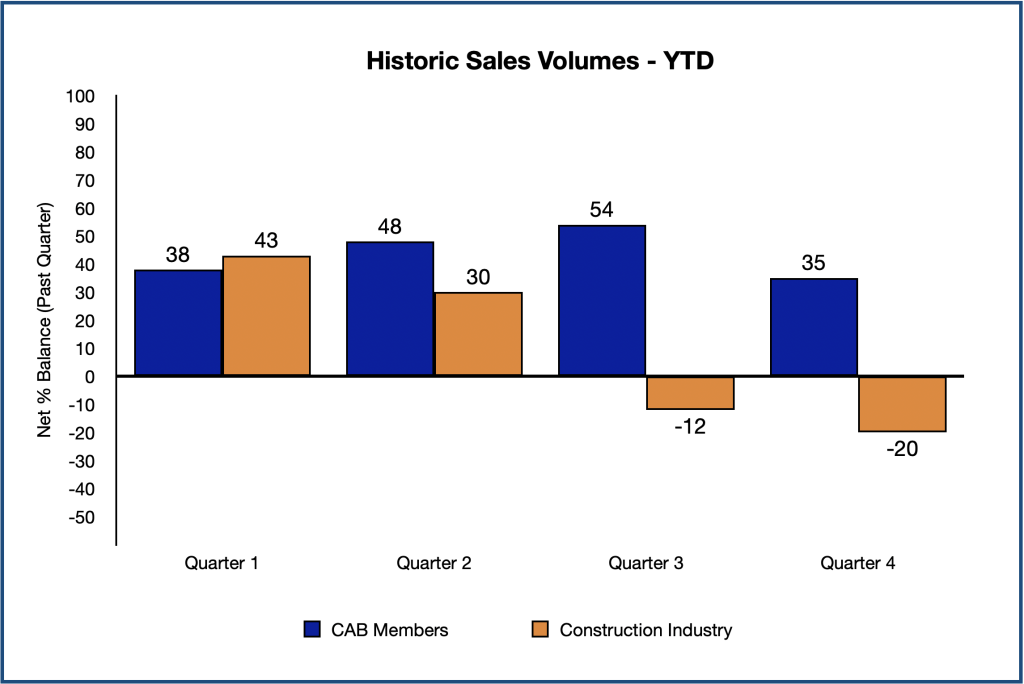

Looking at ‘Historic Sales Volumes’ in 2022 CAB Members have reported on net balance an increase in work for the first three quarters in 2022, with this dropping back slightly in the last quarter. The wider Construction Industry has seen a dramatic change during the year which started at 40% and ended the year on -20% net balance which suggests output has drastically reduced during 2022.

Fenestration installations have always remained relatively buoyant when there is a drop in construction output. This is possibly due to the need to ensure buildings already in construction or refurbishment require fenestration to ensure waterproofing of their envelope. Over a longer downturn output tends to remain positive as replacement fenestration increases as new projects decrease.

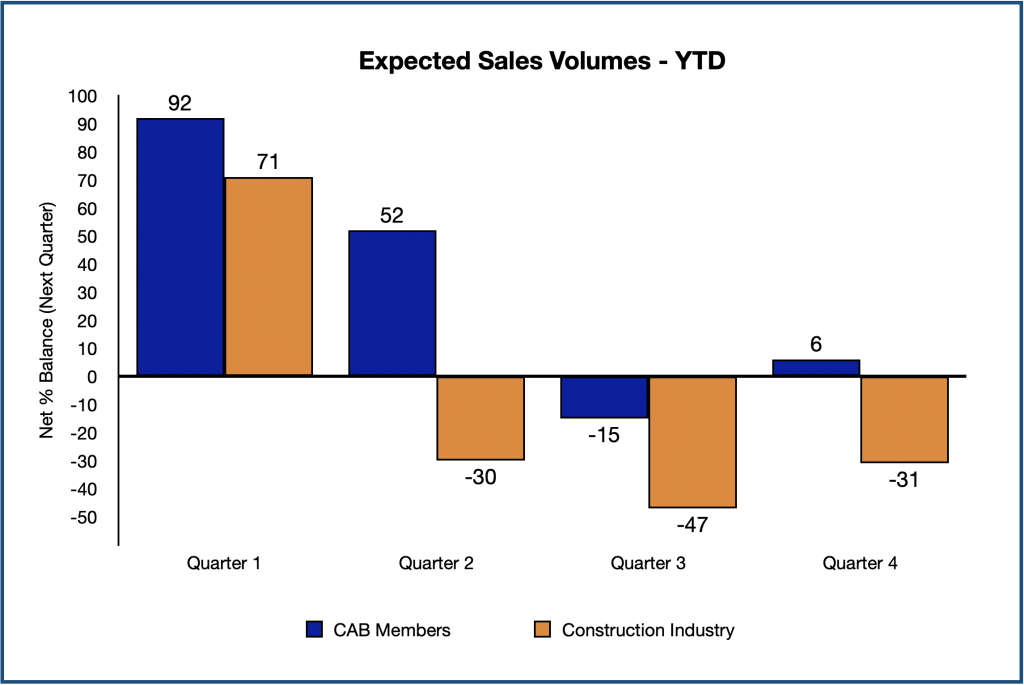

Reviewing ‘Expected Sales Volumes’ the majority of CAB members were positive on net balance at the start of 2022 alongside the wider construction products supply. Members outlook reduced dramatically during the year going negative by -15% in the third quarter only to return up to a 6% on net balance suggesting an increase in Sales revenue for the first quarter of 2023. The outlook for the wider Construction Industry fell much quicker to a low of -47% in the third quarter only to recover to -31% on net balance of respondents.

Whilst ‘Historic Sales Volumes’ during 2022 seem to be continuing to fall on net balance of respondents, the drop is slowing. Couple these results with the forecast of ‘Expected Sales Volumes’ increasing on net balance, we could be seeing a levelling out during 2023 for the construction products supply sector.

Most CAB Members have reported positive ‘Sales Volumes’ during 2022 with some reduction in volumes. In Q4 almost all CAB Members are optimistic for the ‘Sales Volumes’ for the year ahead.

Whilst pressure on ‘Unit Costs’ started the year at 100% on net balance of all respondents, this has softened during 2022 with a further fall in Q4.

As expected, the pressure on ‘Cost Factors’ remains high with the pressure off raw material costs but with energy costs causing the greatest concern followed closely by fuel and wages & salary pressures.

Demand for product continues to dominate the ‘Likely Constraints on Activity Over the Next 12 Months’ for CAB Members. In Q4 this constraint is closely followed by the availability of material supply.

In Q4 27% of CAB Members on net balance are operating at over 90% capacity, when reviewing ‘Historic Capacity Utilisation’. This remains fairly constant throughout 2022. CAB Members see this increasing to 38% in 2023.

For CAB Members ‘Labour Force’ and ‘Labour Costs’ have remained positive on net balance confirming that these is a shortage of experienced and qualified labour. The 94% on net balance 2023 outlook suggests that this is a of growing concern.

Approximately half of CAB Member respondents continue to export product, most only up to 5% of their turnover. Sales exports during 2022 have increased incrementally which is likely due to preferential exchange rates for overseas buyers.

Despite uncertain times during 2022 CAB Members and the wider construction products sector continue to invest most of their ‘Capital Investment’ in renewing plant & equipment and product improvement. As the Construction Industry continues to move towards a zero carbon emission future plant and product changes are needed to keep up with competition and legislation changes. This will continue to evolve in the coming years as legislation continues to force innovation.